All Categories

Featured

Table of Contents

Note, nevertheless, that this doesn't claim anything concerning changing for rising cost of living. On the bonus side, even if you think your option would certainly be to invest in the stock exchange for those seven years, which you would certainly obtain a 10 percent yearly return (which is far from specific, particularly in the coming years), this $8208 a year would certainly be greater than 4 percent of the resulting nominal stock worth.

Instance of a single-premium deferred annuity (with a 25-year deferment), with 4 payment choices. The month-to-month payment here is highest for the "joint-life-only" alternative, at $1258 (164 percent greater than with the instant annuity).

The way you purchase the annuity will certainly identify the answer to that question. If you acquire an annuity with pre-tax dollars, your premium minimizes your taxed income for that year. According to , buying an annuity inside a Roth strategy results in tax-free settlements.

Where can I buy affordable Retirement Income From Annuities?

The advisor's initial step was to create a thorough economic strategy for you, and afterwards clarify (a) how the proposed annuity suits your overall plan, (b) what choices s/he considered, and (c) just how such alternatives would or would certainly not have actually caused reduced or higher settlement for the consultant, and (d) why the annuity is the remarkable option for you. - Income protection annuities

Of program, an expert might attempt pushing annuities also if they're not the most effective suitable for your scenario and objectives. The reason might be as benign as it is the only item they offer, so they fall target to the proverbial, "If all you have in your toolbox is a hammer, pretty soon whatever begins looking like a nail." While the expert in this circumstance may not be underhanded, it raises the risk that an annuity is a bad option for you.

Who should consider buying an Annuity Contracts?

Given that annuities often pay the representative offering them much higher compensations than what s/he would get for spending your money in mutual funds - Secure annuities, not to mention the no payments s/he 'd obtain if you buy no-load shared funds, there is a big incentive for representatives to press annuities, and the extra complex the much better ()

An unethical advisor recommends rolling that quantity right into new "much better" funds that simply happen to carry a 4 percent sales tons. Agree to this, and the consultant pockets $20,000 of your $500,000, and the funds aren't most likely to do better (unless you picked also more improperly to start with). In the exact same example, the advisor might steer you to purchase a complicated annuity with that $500,000, one that pays him or her an 8 percent payment.

The advisor tries to hurry your choice, claiming the offer will soon disappear. It might certainly, but there will likely be equivalent deals later. The consultant hasn't figured out exactly how annuity repayments will be tired. The expert hasn't divulged his/her settlement and/or the fees you'll be billed and/or hasn't shown you the impact of those on your eventual repayments, and/or the payment and/or fees are unacceptably high.

Existing interest rates, and therefore predicted payments, are historically reduced. Also if an annuity is ideal for you, do your due diligence in contrasting annuities marketed by brokers vs. no-load ones offered by the providing company.

Can I get an Annuity Riders online?

The stream of monthly settlements from Social Protection resembles those of a delayed annuity. Actually, a 2017 comparative analysis made a comprehensive comparison. The adhering to are a few of one of the most significant factors. Considering that annuities are voluntary, the people getting them typically self-select as having a longer-than-average life span.

Social Security benefits are fully indexed to the CPI, while annuities either have no inflation defense or at the majority of provide an established percentage annual boost that might or might not make up for inflation completely. This kind of biker, as with anything else that enhances the insurance firm's risk, requires you to pay more for the annuity, or approve lower payments.

How can an Immediate Annuities protect my retirement?

Please note: This post is planned for informational objectives just, and ought to not be taken into consideration monetary advice. You should seek advice from an economic expert before making any major monetary decisions.

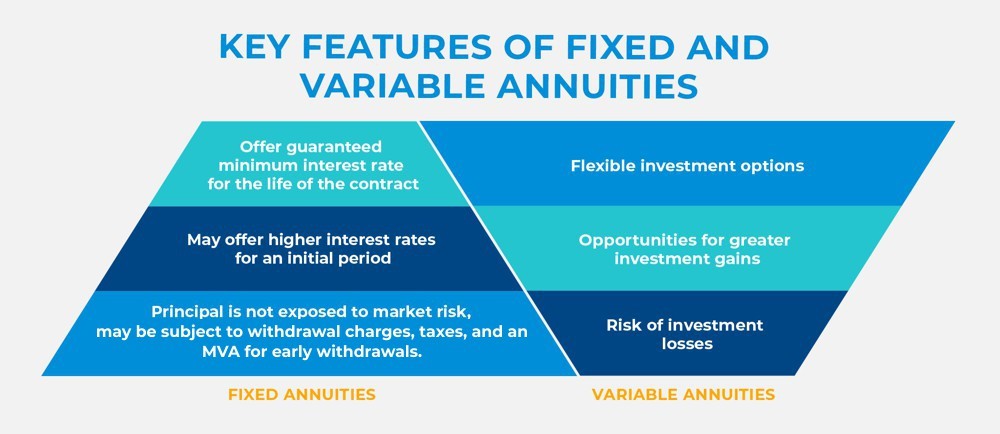

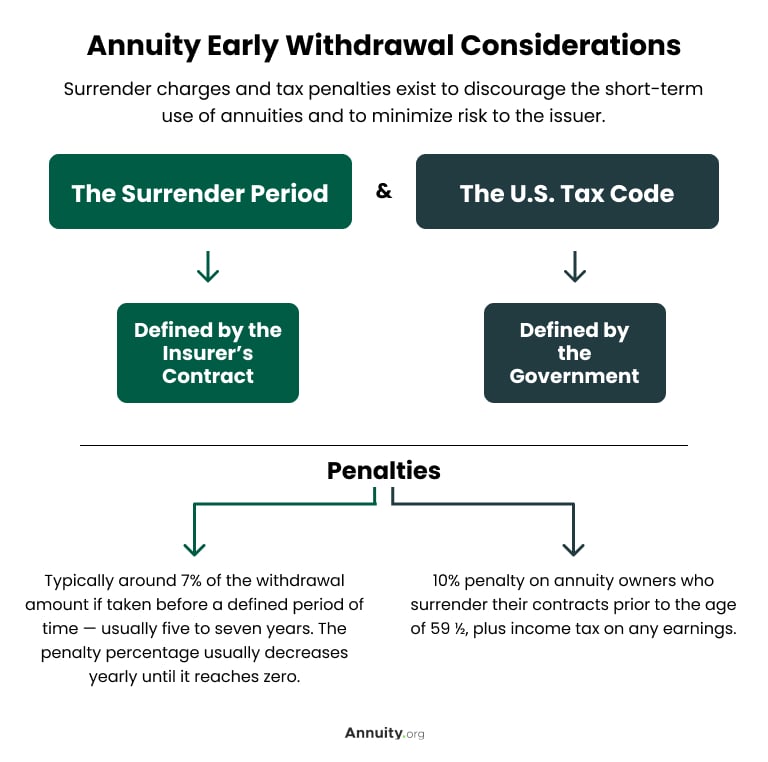

Since annuities are planned for retirement, tax obligations and penalties may apply. Principal Defense of Fixed Annuities. Never shed principal as a result of market efficiency as fixed annuities are not purchased the marketplace. Also throughout market recessions, your money will not be impacted and you will not shed money. Diverse Investment Options.

Immediate annuities. Deferred annuities: For those that want to expand their money over time, yet are prepared to defer accessibility to the money till retirement years.

Are Long-term Care Annuities a safe investment?

Variable annuities: Offers greater potential for growth by spending your money in financial investment options you choose and the capability to rebalance your profile based on your preferences and in a way that aligns with transforming monetary objectives. With repaired annuities, the company invests the funds and provides a rate of interest to the client.

When a death case happens with an annuity, it is essential to have a named recipient in the contract. Different alternatives exist for annuity fatality advantages, relying on the contract and insurance company. Choosing a reimbursement or "period certain" option in your annuity offers a death benefit if you die early.

Why is an Guaranteed Income Annuities important for long-term income?

Calling a recipient other than the estate can help this procedure go extra efficiently, and can assist make certain that the earnings go to whoever the private wanted the money to go to rather than going via probate. When present, a fatality benefit is immediately consisted of with your contract.

{kind=link}

Table of Contents

Latest Posts

Decoding How Investment Plans Work A Comprehensive Guide to Fixed Annuity Vs Equity-linked Variable Annuity What Is Fixed Annuity Or Variable Annuity? Benefits of Choosing the Right Financial Plan Why

Breaking Down Your Investment Choices A Comprehensive Guide to Investment Choices Breaking Down the Basics of Fixed Indexed Annuity Vs Market-variable Annuity Advantages and Disadvantages of Different

Analyzing Annuities Variable Vs Fixed A Comprehensive Guide to Investment Choices What Is Choosing Between Fixed Annuity And Variable Annuity? Features of Smart Investment Choices Why Fixed Income Ann

More

Latest Posts